At a recent European Digital Banking Summit, our CTO Kevin Collins told an anecdote from his personal experience that underlines the threat to incumbent banks posed by the challengers.

As he was travelling so often to overseas conferences and events, he had set up a Revolut account (free foreign exchange transactions were a compelling draw for many of the company’s early adopters). Although he had maintained a solid relationship with the same bank for most of his life, as most of us do, he became increasingly frustrated with the irrelevant offers and content being sent to him.

For example, he would regularly receive promotional information about the latest mortgage rates. His bank had somehow missed the large, monthly payment that had been going out of his account for years marked “Mortgage”.

The relationship began to break down little by little and gradually Revolut became the most used card in Kevin’s wallet.

One day he logged into his “traditional” bank account and saw this message “No transactions”. Yet, all of his money was still there. He hadn’t closed the account, nor had he any intention of doing so.

At that moment, came a realisation. It isn’t simply losing accounts to the challengers that should worry established banks. In fact, there is plenty of evidence to suggest that the vast majority of us will, at the very least, continue to keep these accounts to receive salary payments, amass savings and pay off mortgages and loans.

No, the real war is for customer data. And in this instance, “No transactions” was the white flag of surrender.

When banks no longer have this fundamental data, because their customers are using Revolut, Monzo et al to pay for goods and services on a day-to-day basis, they lose the ability to engage them with relevant content. They don’t have the raw material to add value to their customers’ experience.

And they can no longer influence them towards business goals.

But here’s the kicker; when the customer experience they provide is good, banks are swimming in relevant, engaging data. It’s the kind of information that CRMs in other industries are desperate for.

In part one of this series, we looked at the topic of digital transformation in the banking sector as a whole and considered the lofty task of revolutionising your core banking system. Now, we’re going to focus on how you can meet the neo banks head-on, create exceptional customer-centric experiences and hold on to that all-important data.

Mini case study– DBS, Singapore

In the May 2019 edition of The Economist, Piyush Gupta, the Chief Executive of DBS (the biggest bank in Singapore) revealed a personal eureka moment. Speaking about the rise of Ant Financial (the highest valued fintech company in the world and an affiliate of Alibaba), he said

In other words; all of the perks, without the hard work. This observation, made in 2014, convinced him that he needed to act fast if his bank was to survive as more than a water carrier for the challengers. DBS embarked on a root and stem digital transformation.

In April of this year, the managing director and group head of institutional banking at DBS, Tan Su Shan, spoke about the scope and success of this project. At its core was an agile task force charged with creating an open application interface system (API), which would allow the bank to partner with cutting-edge technology service providers who could lend their expertise and functionality to the DBS platform.

The upshot of this? A varied range of third-party services to avail of, combined with an exceptional user experience for its customers. As a result, the DBS marketplace, made possible by the API, earns the bank considerable commission on the cars, properties and home-energy contracts sold through it. In fact, according to Gupta, online customers are over 30% more profitable than regular banking clients.

This is an important point to note. For all of its incredible in-house upgrading, including the migration of 80% of its computer processing away from core legacy systems and onto the cloud, DBS knew what it should outsource. Why would you build a real estate marketplace, for example, when you could simply plug in a ready-made solution?

It’s undoubtedly more cost-effective, for a start. And a lot faster.

Time is of the essence

Recently, Bank of Ireland, one of our long-standing clients, announced details of a five-year transformation project to replace its core system with the Temenos solution. Given the scope of the task, the time frame is not unusual.

However, not every upgrade requires this amount of time, or resources, to implement. The front-end experience and the flashy, eye-catching service features that consumers have come to expect from their banks can be put in place at a fraction of the price and within a matter of months.

Around the world, banks are investing huge resources into the stuff “under the bonnet”, and rightly so. Yet, whilst this is essential for ensuring their long-term stability, it doesn’t strengthen the bond between the banks and their customers in the short term.

Which banks are getting the customer experience right?

In Australia, ING (an online-only bank) embarked on a two-year plan to reinvigorate its digital platform. They enlisted the help of 16,000 customers to shape the roadmap, putting the focus squarely on creating better experiences for the people that matter most. Although ING is not immune to technical problems (it was amongst a number of banks affected by an outage recently), its priorities are fundamentally right.

They’ve put a huge emphasis on reducing churn. How so? They utilise behavioural analytics, leveraging its rich customer data to personalise communications. This eliminates irrelevant offers that would otherwise damage the relationship between ING and its customers.

Instead, ING is automating its marketing and sales campaigns, intelligently targeting customers with relevant offers across its website and mobile app.

The result? A 120% increase in conversions and a 45% year on year rise in cross-sell purchases.

Customer-centric experiences demystified

So, how do you emulate this success without investing in a two-year project and recruiting your customers to point you in the right direction?

To deliver personalised, customer-centric experiences quickly, banks need agile service partners that can be “plugged in”, similar to what DBS did to build up its marketplace, and utilised to execute core business goals at scale.

Xtremepush has been leading the way in this regard since 2015, working with a range of tier one banks around the world to enhance their customer experiences. Our next-generation platform combines enterprise-grade behavioural analytics with a full suite of engagement channels (across web, app, email, SMS and social messengers). The platform is also modular, allowing banks to roll out the most valuable use cases within a matter of months. From here, additional channels can be added as the need and opportunities arise.

In terms of keeping pace with, and even outperforming, the neo banks, let’s look at three core use cases, each driving a specific, customer-focused business goal; acquisition, engagement, retention.

Onboarding app users

The focal point of modern banking is the app. Initially, it was simply a convenient method of checking one’s balance, but now customers expect it to provide a full range of banking services. It is arguably the most important engagement channel in a bank’s arsenal.

Yet, how many of your customers fail to get beyond the initial login screen and give up? On average, the figure stands at 20% but can be much higher depending on the quality of the experience.

We empower banks to create frictionless onboarding experiences that intelligently nudge the user towards goal completion. We also provide the analytics required to identify and address the drop-off points.

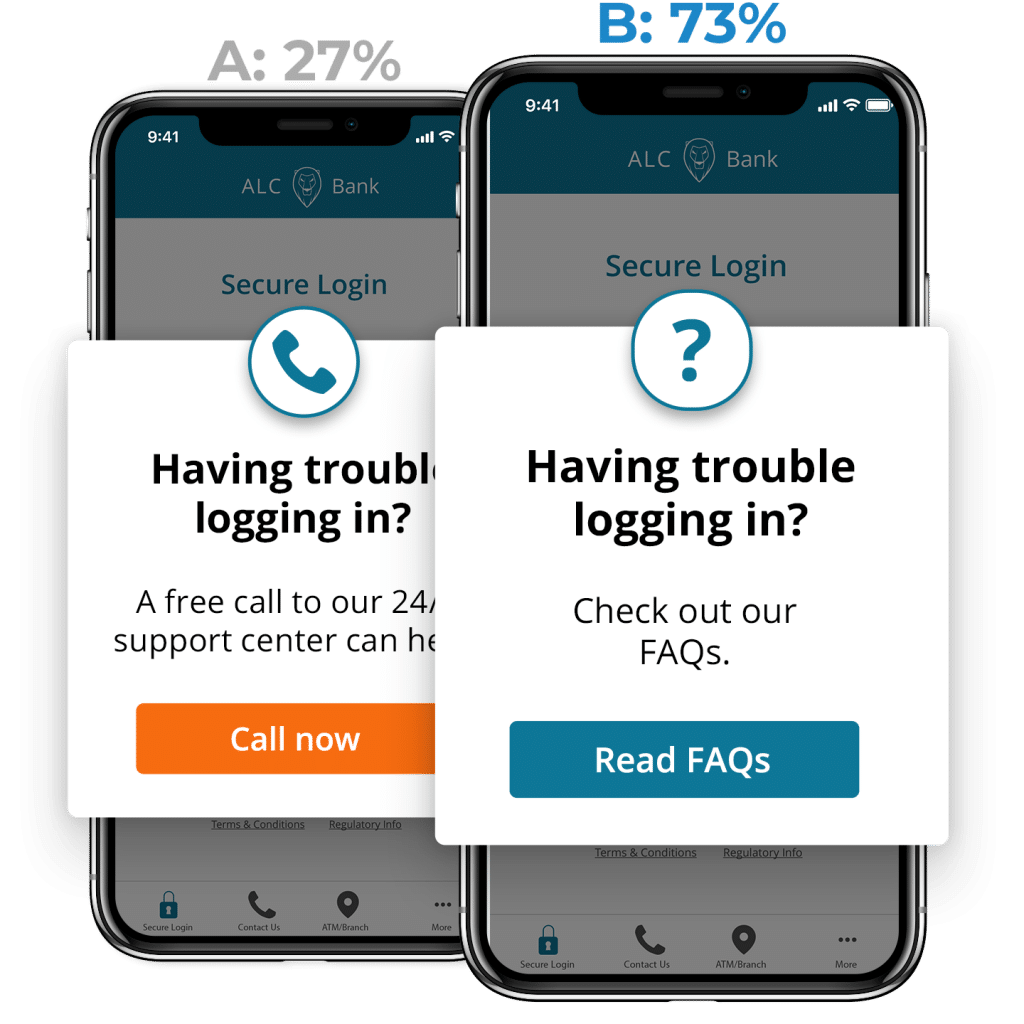

In this example, an automated in-app message has been sent to a user who has failed to log in on during their second session. The content has also been A/B tested to optimise conversion rates. One of the banks we work with actually increased their number of registered app users by 7% using this strategy.

Personalised, real-time engagement

Push notifications are how the likes of Revolut instantly inform customers about account transactions, for example, when a customer’s direct debit has gone out or when a salary payment has been received. These are real-time, event-triggered notifications delivered directly to a customer’s mobile device or desktop.

This might seem complicated but in fact, it’s easily achieved. We’ve already helped traditional banks roll these campaigns out.

Encouraging online applications

The number of loan and mortgage applications made online is increasing year on year. It’s faster and a lot more convenient for the customer.

Unfortunately, applicants can be easily distracted or become disinterested during the lengthy application process. Our clients possess the ability to re-engage their customers at a later time and bring them back to the exact point they left off at.

We had a tier-one client exceed its yearly loan book target by 150% within 9 months using this strategy. That’s the value of smarter, personal engagement.

You can also layer propensity-to-loan data into these campaigns so that you only attempt to re-engage applicants who are likely to be successful.

The next steps

These use cases are only the tip of the iceberg. We’re also helping banks to automate ForEx messaging for customers who travel overseas, intelligently segment their card-linked offers by demographic and behaviour and even combat card fraud.

If you’re interested in learning more about how to deliver relevant, engaging customer experiences across every channel, we’ve actually actually written a multichannel playbook specifically for the banking industry. You can download it here.

Alternatively, you can get in touch with us directly and schedule a demo of the platform.